This past February, we at #ANGELSchallenged the tech industry to talk about, measure and fix #TheGapTable. The cap table — the document that records who has ownership in a startup — holds the roadmap to power in Silicon Valley. Cap table wealth enables individuals to fund the next generation of products and institutions that shape our industry — and increasingly the world — through investing, starting a venture firm, founding a startup or funding political and philanthropic campaigns. We called it #TheGapTable because we suspected that women have a disproportionately low share of startup equity and capture just a fraction of the industry’s wealth creation. We now have the data to prove it, thanks to Carta.

Carta is the leading software platform for managing equity and ownership. Their mission, to democratize access to ownership, resonates with our mission to get more women on the cap tables of successful startups. Carta offered to team up to analyze their broad and deep set of anonymized, aggregated equity data¹. We believe this is the first comprehensive public study of cap table data by gender.

Carta analyzed cap table data from more than 6,000 companies with a combined total of nearly $45 billion in equity value². Carta analyzed this data to understand how equity is allocated by inferred gender amongst founders and employees — we also hoped to analyze equity by non-binary gender and by ethnicity but Carta does not yet collect this data³. For simplicity, we started with founders (who control the cap table) and employees (the majority of shareholders), but we hope that further research delves into venture capital⁴ (where we know women make up just 9% of check-writing investors), angel investors, board members, advisors and other entities on the cap table. Please read Carta’s full research report, which includes details of the methodology, here.

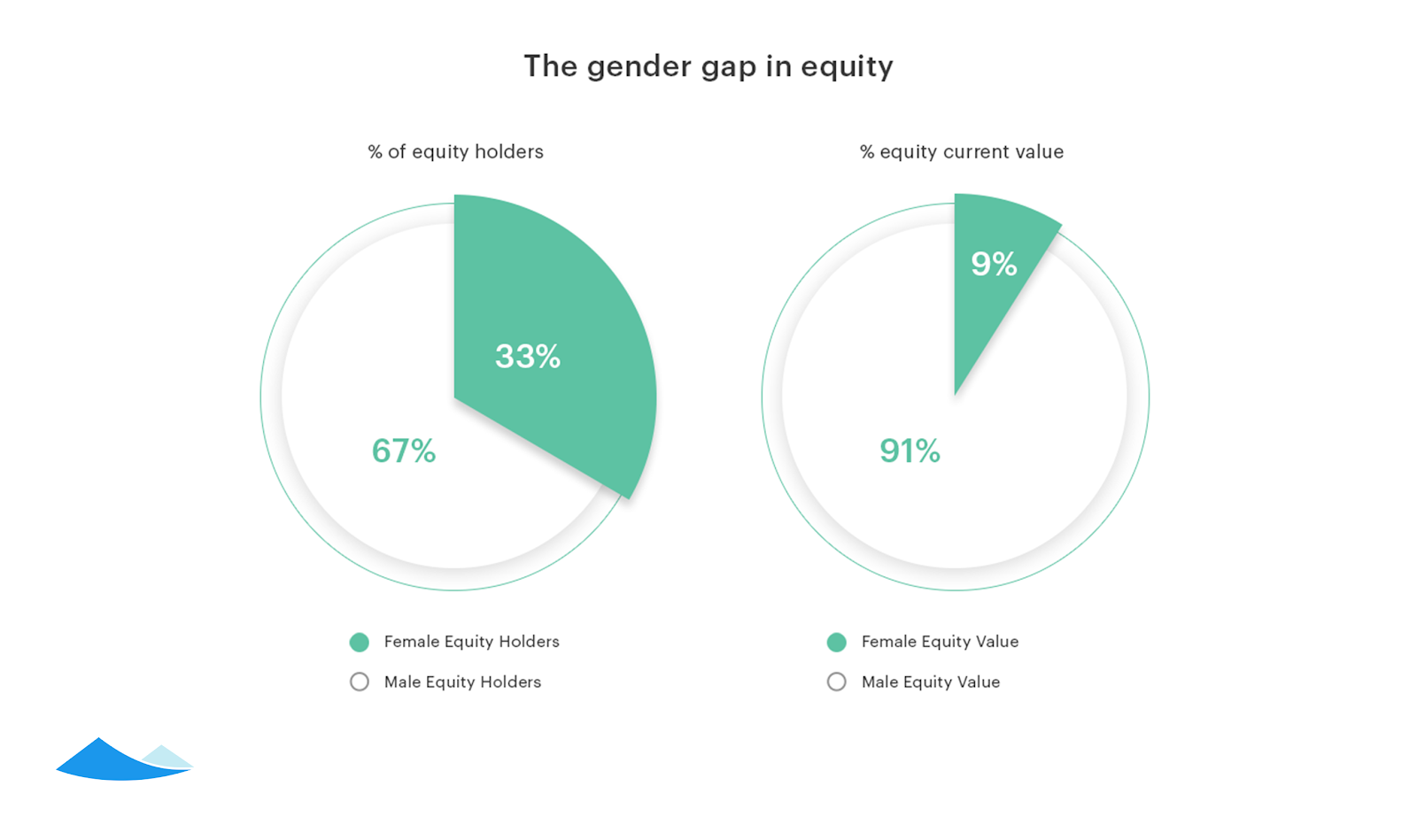

So what did we learn? The equity gap in startups is real. Women make up 33% of the combined founder and employee workforce but hold just 9% of the equity value. The other 91% belongs to men.

Let’s break it down by founders and employees:

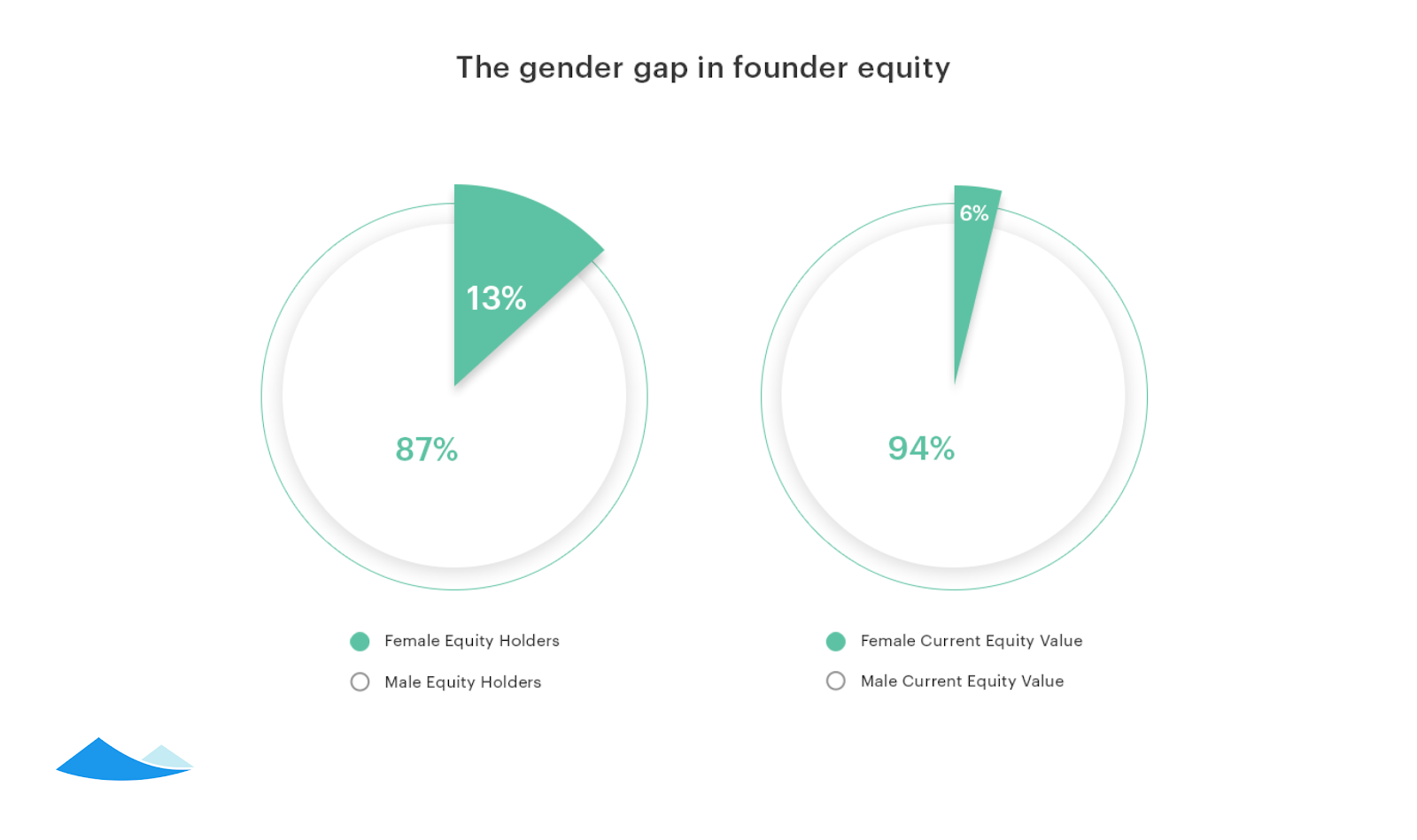

- Founders: women represent 13% of all founders but own just 6% of all founder equity value. In dollars, the average female founder on Carta owns just 39¢ in equity for every $1 that the average male founder owns.

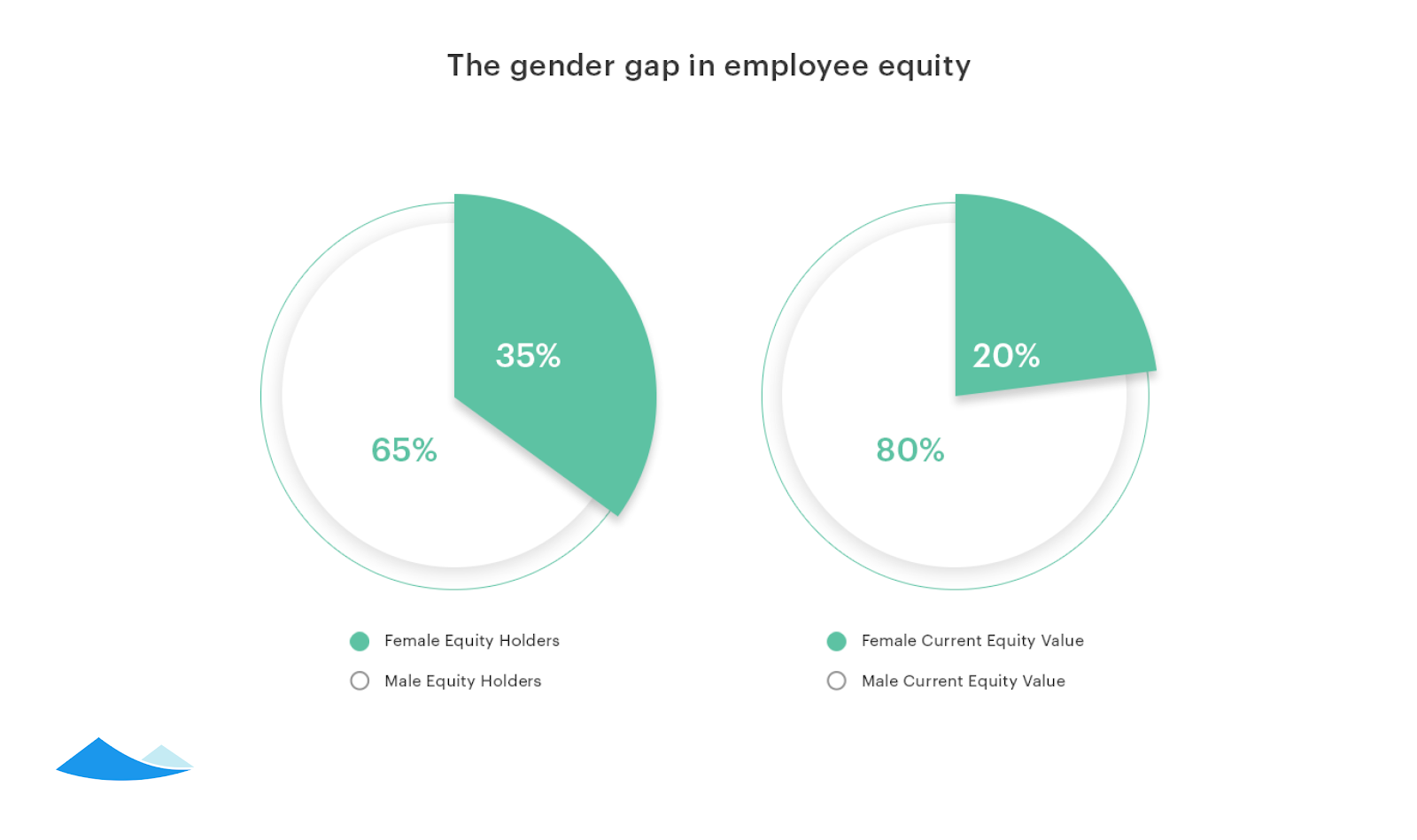

- Employees: women make up 35% of all employees who hold equity, but capture just 20% of the employee equity value. In dollars, female employees on Carta make just 47¢ for every $1 of equity male employees get.

Despite these findings, it’s important to note women do not have a universal shared experience in the tech industry. Women of color, particularly underrepresented minority women, face significantly more harassment, bias and barriers in our industry. This reality, combined with decades of research into the pay gap, lead us to believe that white women capture the majority of the 9% of equity value held by women in the startup industry.

Founders:

That women make up just 13% of founders is a well-known problem, but the equity discrepancy suggests that female founders’ firepower to change this reality is also severely limited.

How to explain this massive gap? It’s likely a combination of complex, interrelated factors. Our hypotheses focus on valuation and dilution, capital raised, allocation of equity, bias and performance but further investigation is necessary to better understand the primary drivers for this disparity:

- Lower valuation and higher dilution: female founded companies may be raising money at lower valuations and giving up a greater proportion of their company to investors, diluting founder equity. A recent study by Quartz and Pitchbook of the top 350 startups found that female-led companies were indeed valued an average of just 16% of male-led companies, suggesting that this may be a primary driver of the equity discrepancy. Valuations of private tech companies are subjective, particularly in the early stages of development and prone to bias.

- Less capital for women: female-founded companies are under-funded in comparison to male-founded companies. According to Pitchbook, startups with at least one female co-founder made up 20% of all venture deals in 2017, but secured 15% of all funding. The discrepancy comes almost entirely from all-female founding teams, which made up 5% of all deals but captured just 2.4% of venture funding.⁵ And black female founders have received just a tiny fraction of funding (0.0006% of all venture funding since 2009). If this disparity is due to lack of access to adequate capital, it may handicap female founded startups’ growth and ability to compete.

- Investor bias: investors treat female founders differently, from biased responses to their pitches to discrimination in the perceived capabilities and barriers to success for female founders. In a 2017 study published in the Harvard Business Review, researchers found that venture capitalists (both male and female) posed different types of questions to male and female entrepreneurs — they asked men questions about the potential for gains and women about the potential for losses — which, after controlling for other factors, entirely explained the funding gap between male and female founders. In fact, it led to seven times less funding. Women are also often penalized for the very traits — confidence, aggression — that investors seek in founders.

- Industry bias: women may found companies in fields that are perceived as lower value — for example, creating communities, services or marketplaces powered by less cutting edge technology or in fields considered less compelling (like fashion, parenting) compared to the ones currently capturing venture capital attention (like cryptocurrency, artificial intelligence). Quartz found that women are almost twice as likely to start healthcare and consumer businesses, while men were far more likely to start financial services and enterprise companies. But we also know that fields that are male dominated are ascribed higher value often simply because they are male dominated, and that those identical fields lose their value when they become female dominated. For example, computer programmers were predominately female and made modest wages in the early decades of the profession, until men took over. We also know that male dominated fields create barriers to attracting and retaining women.

- Investor underrepresentation: women are vastly underrepresented in venture capital, and investors tend to invest within their networks and in people who look like them.

- Negotiation: women face well-known challenges in negotiation, which may impact the valuations they achieve, the ownership they retain (dilution), and total capital raised. This can also be due to a lack of data and benchmarks required to negotiate well — thanks to the absence of robust entrepreneurial networks — as well as to socialized risk aversion, which results in women asking for less funding than they need or than their peers.

- Allocation of equity: female founders may tend to have more co-founders than men, splitting founder equity amongst more people. Female founders may be awarded less equity than their male co-founders due to differences in roles (for example, women may be less likely to be CEO although Quartz’s analysis suggests that’s not likely the case), or to discrimination. Female founders may also set larger reserves for employee equity pools than male founders, thereby decreasing their shareholdings.

- Performance: due to the factors above, and the bias female leaders face, female-founded companies may not grow as fast or as large as male-founded companies.⁶ According to Crunchbase, female founded companies drop from 19% of all seed and angel stage companies to 12% of Series C or later companies. The gap in equity suggests that female founders may not be set up for success due to raising smaller rounds at lower valuations, often competing on shorter runways due to underfunding (with higher expectations), while not getting the same levels of support or access as male-founded companies.

Each of these hypotheses about the gap in female founder equity needs further research. In the meantime, for the average female founder — who sees herself underrepresented amongst funders and founders — her ability to change this reality by investing in the next generation of startups or becoming a backer for a new generation of investors is limited to 6% of the potential wealth creation of founders. The downstream effects of this wealth gap in our frontier industry are significant.

Employees:

Women make up approximately 35% of equity-holding employees on Carta, but hold just 20% of the employee equity value. Female employees make just 47¢ for every $1 of equity male employees get.

Compared with the wage gap⁷, the equity gap is far worse⁸. Overall in the US, women make up almost half the workforce and earn 80¢ for every $1 that men earn, though this varies widely by ethnicity, with Asian women earning 87¢, white women earning 79¢, black women earning 63¢ and Latinas earning just 54¢ of what white men make in salary. When it comes to wealth creation, we are stuck in the 1960s.

What is causing this gap? Similar to the wage gap, it’s likely a set of factors, but a primary driver is that women are underrepresented in the three employee groups that get significant equity allocations:

- Early employees: a startup’s earliest team members get the lion’s share of the employee equity and at the lowest prices, leading to the greatest wealth creation. According to Carta, women represent 29% of employees in companies with up to 10 employees, and only get to 44% representation when companies have over 500 employees.

- Engineers: women usually make up less than 20% of technical roles at later stage tech companies. Engineers are given more equity than non-technical employees (i.e. marketing, sales, operations, support or HR functions, which skew female), and they represent more of the first employees than other functions. (It may be worth considering how equity is awarded across functional areas.)

- Senior leadership: women make up about 11% to 25% of leadership roles in later stage tech companies.

The intersection of these three areas likely compounds the problem, resulting in even lower representation of women as early engineers and early leaders, which may explain the discrepancy between employee representation and their equity.

Just like female founders, female employees may also face similar challenges with underrepresentation in decision-making roles, bias against women in power, and negotiation. This may lead to equity being allocated unequally between men and women in the same roles — just like salary (tech leaders like Salesforce have been surprised to find persistent wage gaps). We need further research that examines equity allocations by title and role to understand this.

What can we do?

When men capture the overwhelming majority of the financial outcome of successful startup exits, they shape the next generation of companies, products, politics and philanthropic endeavors.

Now that we know about #TheGapTable, CEOs and investors need to measure, publish and fix it. And the whole industry has a role to play in making conversations about equity common, accessible, and transparent. Carta has made the first step easy. It’s now possible to measure your cap table by any demographic you choose, including gender, non-binary gender, race and ethnicity by using their new tool.

Founders & CEOs: Henry Ward, Carta’s CEO, has a refreshingly honest and action-oriented take on why #TheGapTable matters and how to fix it. As he states, “CEOs have to be the driver of these conversations — nobody else will.” Follow Carta’s excellent example by measuring and fixing your own gap table. Carta’s tool makes it easy. For founders just getting started, co-found companies with women — and not just white women. Raise money from women investors. Hire women from day one. Compensate men and women equally when in similar roles. And focus on women of color, especially URMs (underrepresented minorities), in all these areas as they face even higher barriers in our industry.

Investors: you control who gets capital and at what terms. Fund women and URMs. Give them fair and equal terms. Be honest and aggressive in understanding your own biases in who you fund and how you value their companies. Help your male founders recruit women into early and executive roles and invite women investors into your deals. Recommend your startups measure #TheGapTable. And finally, measure and publish the diversity of the founders you fund and the capital you deploy.

Employees: ask your CEO to measure and talk about the diversity of your company’s cap table. Educate yourself on equity and how to best value and benchmark it (Carta’s equity 101 guide is excellent). Discuss and benchmark your offer with people you trust; ask counterparts to share their equity and compensation information.

People with Privilege: one of the best ways to be an ally is to proactively talk about your equity and compensation with women and URMs so they can better negotiate for parity. Ask your manager how your own equity compares to women and URMs in similar roles; investigate any discrepancies. Ask your employer to share and talk about your company’s gap table.

#TheGapTable analysis is a watershed moment. We are grateful to Carta’s leadership and efforts to bring transparency to what was previously opaque. This analysis is the first of its kind but it must not be the last. As an industry, we need to ensure that a diverse set of people, who see the full range of possibilities and problems, are able to shape the products and institutions of Silicon Valley, and beyond. We can’t talk about equality in Silicon Valley without talking about equity. We’ll never have an equal seat at the table until we close #TheGapTable.

—

Our mission at #ANGELS is to get more women on the cap tables of successful startups. In addition to investing, we curate events and conversations through #ANGELS Access to build community, diversify networks, and include and promote women in frontier fields shaping the industry. Sign up for our #ANGELS Access events here.

—

- #ANGELS never had access to Carta’s data, but collaborated with Carta on methodology for this analysis.

- These 6,000 cap tables include over 180,000 employees and 15,000 founders. Carta clients represent a range of venture backed startups across technology, including consumer, e-commerce, biotech, gaming and beyond. Carta’s dataset skews heavily towards early stage, pre-exit startups (companies on Carta have an average company size of 34 employees and average age of just under 5 years old), so while these findings are an important leading indicator of #TheGapTable, future analyses that include more mature companies may shift findings to reveal more or less equality.

- Carta does not currently collect gender or ethnicity information, and while Carta & #ANGELS recognize that gender is non-binary, Carta assigned gender by categorizing names using data from the U.S. Social Security Administration which does not allow for non-binary gender categorization. Carta has released a feature that allows companies to track any stakeholder demographic they choose, from non-binary gender to ethnicity and race. Carta hopes this study will inspire companies to run their own analysis.

- Venture funds typically retain 20–30% of the upside of their funds and women make up only 9% of check-writing investors at these funds. The other 70–80% of the returns go to the venture funds’ LPs (Limited Partners) which are typically pension funds, university endowments and family offices, for which it is nearly impossible to track gender. For information about gender equality in venture capital, please see The Information’s VC Diversity Index and the data All Raise has collected.

- Amongst companies where gender could be determined.

- This study does not account for female founded companies potentially failing sooner or more often than male founded companies. Carta only included companies that are currently operating in the study.

- It’s worth understanding what the wage, or pay, gap represents. It is not a measure of the difference in pay for men and women doing identical work (“equal pay for equal work”). While it does capture such discrimination, it also reflects differences in fields, jobs, seniority, hours worked, education, experience, and other choices and constraints that people have in their careers. Of course, many of these differences are the result of discrimination and socialization, including the fact that women work fewer paid hours because they provide more unpaid hours in caregiving compared to men. Similarly, the equity gap captures a host of factors. This article is a great resource for understanding the complex factors the pay gap captures.

- The pay gap uses the median to analyze the gap in earnings between men and women. Carta uses the mean to measure the equity gap. Using the same methodology at the pay gap — the median versus the mean — the equity gap for female employees remains similar at 53¢ (versus 47¢ at the mean) for every $1 of equity a male employee earns. Why two different approaches? The goal of the pay gap is to capture the experiences of the average working person, hence the use of the median or mid-point of earnings. In venture-backed technology businesses, the vast majority of startups fail, and very few make outsized returns. It’s only the outliers that create the wealth and power that shape the rest of industry. Hence, using the mean (which captures the outliers) is the appropriate methodology for an equity gap study.

- Bitcointalk:

- https://bitcointalk.org/index.php?action=profile;u=1582803;sa=forumProfile

Tidak ada komentar:

Posting Komentar